For a 0.24% management expense ratio (MER), you get an all-in-one mix of 80% global stocks and 20% bonds, rebalanced periodically, with a Canadian home bias to improve tax efficiency and reduce currency risk. Despite its growth bias, it pays a not inconsiderable quarterly dividend. If imitation is a form of flattery, VGRO comes highly praised: there are now copycats out there from other providers—XGRO, ZGRO, TGRO, HGRW—all with lower MERs.

VGRO holdings

What stocks does VGRO have?

- Vanguard U.S. Total Market Index ETF 35.14%

- Vanguard FTSE Canada All Cap Index ETF 24.65%

- Vanguard FTSE Developed All Cap ex North America Index ETF 14.44%

- Vanguard Canadian Aggregate Bond Index ETF 11.83%

- Vanguard FTSE Emerging Markets All Cap Index ETF 5.47%

- Vanguard Global ex-U.S. Aggregate Bond Index ETF (CAD-hedged) 4.23%

- Vanguard U.S. Aggregate Bond Index ETF (CAD-hedged) 4.21%

As of April 30, 2025

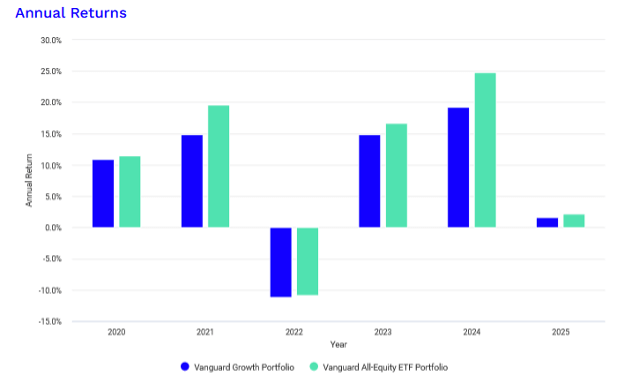

The VGRO ETF and its peers aren’t perfect, nor are they as “safe” as some Canadian investors might assume. In fact, during 2022, VGRO’s price fell 11.19%, a deeper drawdown than its 100% stock counterpart, the Vanguard All-Equity ETF Portfolio (VEQT).

That’s because VGRO’s 20% bond sleeve, typically a buffer against stock losses due to its usual negative correlation, also dropped sharply in the face of rising interest rates. The average duration of VGRO’s bond holdings is 6.8 years, which means it’s fairly sensitive to rate hikes. All else being equal, a 1% rise in rates could lead to roughly a 6.8% price decline in the bond component alone. And in 2022, this occurred during an equity bear market, exacerbating losses for VGRO.

If you’re concerned about a repeat of this scenario—where both stocks and bonds fall together—there are ways to shore up VGRO’s weaknesses, or that of any stock-and-bond-based portfolio. Here are two TSX-listed ETF ideas worth considering, along with the trade-offs and what you’ll want to watch out for.

With the Bank of Canada holding rates steady at 2.75%, investors still have the option to keep some cash reserves in their portfolio earning a decent yield without taking on meaningful risk. Cash is a viable asset class. It doesn’t have the equity risk of stocks, and it avoids the credit or interest rate risk you get with bonds. When both stocks and bonds fall at the same time, cash is one of the few things that still holds its value.

In those moments, cash is king and far from being a dead weight. In fact, Warren Buffett (or rather his successor, Greg Abel) holds nearly $350 billion worth in Berkshire Hathaway. That said, there’s a smarter move than simply leaving money sitting in your brokerage account.

I prefer something like the Global X 0–3 Month T-Bill ETF (CBIL). This ETF invests in ultra short-term federal government-issued treasury bills and essentially returns the Bank of Canada’s policy rate minus its fees. With a 0.11% management expense ratio, the ETF currently yields about 2.58% annualized.

It’s also highly liquid, with a one-cent bid-ask spread and minimal price fluctuation. The way it works is simple: its price ticks up slowly throughout the month, then drops slightly on the ex-dividend date by the amount of income earned that month—like a sawtooth pattern.